Inside Japan’s AI-Powered On‑Chain Finance Revolution

Discover how Japan is building AI-driven, blockchain-based finance with digital yen, megabanks, and autonomous agents that could redefine global money and settl

Discover how Japan is building AI-driven, blockchain-based finance with digital yen, megabanks, and autonomous agents that could redefine global money and settl

Japan’s experiment with AI in finance is not just about smarter chatbots or faster customer service; it is about allowing autonomous systems to initiate, verify, and settle real transactions. Instead of waiting for traditional banking hours or manual approvals, AI agents could move funds across approved digital payment rails when predefined conditions are met. For businesses, that could mean suppliers are paid the moment inventory is delivered and verified. For consumers, it could mean bills, subscriptions, and savings transfers are handled automatically with clearer rules and stronger oversight. The bigger story is that Japan is testing how money behaves when financial decisions can happen continuously, securely, and at software speed.

By 2026, Japan’s on-chain finance strategy points toward a financial system that runs continuously on blockchain-based infrastructure. This means payments, settlements, compliance checks, and contract execution could happen 24/7 instead of being limited by bank schedules or legacy batch processing. In practice, an exporter could receive payment automatically when shipping data confirms delivery, while an insurer could release funds once a verified claim condition is met. AI agents would act as the decision layer, while blockchain rails provide transparency, traceability, and programmable execution. Understanding this shift is essential for anyone tracking the future of digital payments, tokenized assets, and automated commerce.

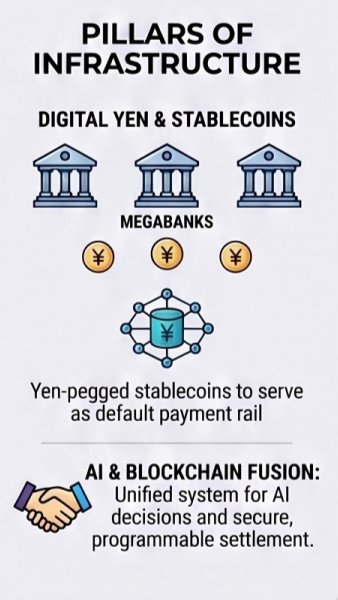

Japan’s financial transformation is less about launching one flashy digital product and more about building a programmable money infrastructure. Megabanks, digital yen initiatives, and settlement networks could work together to create rails where transactions are verified and cleared in seconds. For example, a corporate treasury system could automatically convert, allocate, and settle funds across subsidiaries without waiting for manual banking workflows. Programmable settlement also opens the door to conditional payments, where money moves only when compliance, delivery, or identity checks are satisfied. This could make Japan’s financial system more efficient while giving regulators better visibility into how digital transactions flow.

Autonomous AI agents could become the invisible operators behind supply chains, procurement systems, and even household finance. In a manufacturing scenario, an AI agent might reorder materials, confirm supplier credentials, trigger a smart contract, and release payment once delivery data is validated. At home, similar systems could optimize utility payments, loan repayments, and savings transfers based on real-time income and spending patterns. The benefit is not simply convenience; it is the removal of repetitive financial bottlenecks that slow down everyday decisions. Still, strong permissions, audit trails, and regulatory oversight will be essential to keep automated finance accountable.

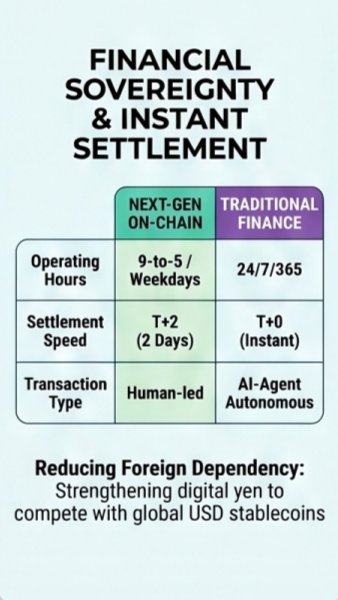

Japan’s push into digital yen and on-chain finance could give it a stronger position in a global market increasingly shaped by dollar stablecoins. Today, many digital asset transactions rely on dollar-based tokens, which can increase dependence on foreign currency infrastructure. A programmable digital yen could support instant settlement, domestic liquidity, and AI-led transactions without routing everything through dollar stablecoin networks. For Japanese businesses, that may reduce currency friction in local commerce and create new options for cross-border trade. Strategically, this is about monetary competitiveness as much as payment innovation.

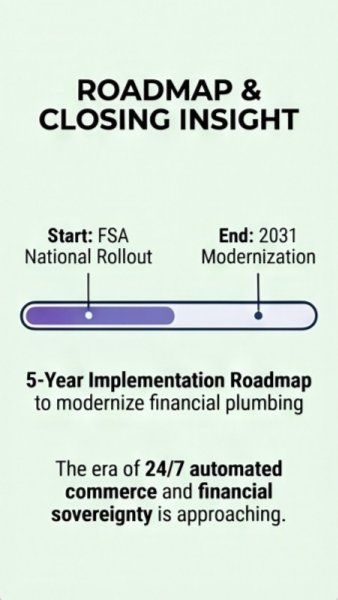

Japan’s five-year roadmap signals that machine-speed finance is moving from theory into implementation. As AI agents, blockchain rails, and programmable settlement mature, companies will need systems that can respond to transactions in real time. Finance teams may have to rethink approvals, reconciliation, compliance monitoring, and liquidity planning for an always-on environment. Consumers will also need clearer controls over which automated services can move money on their behalf. The winners will be the organizations and individuals that prepare early for a financial system where delays are exceptions, not defaults.

Discover more insights and resources on our platform.

Visit Kryptomindz