How Stablecoins Are Rewiring Global Finance

Discover how stablecoins, tokenized deposits, and CBDCs are reshaping global payments, cutting costs, and building the internet’s next financial backbone.

Discover how stablecoins, tokenized deposits, and CBDCs are reshaping global payments, cutting costs, and building the internet’s next financial backbone.

Stablecoins have evolved from a niche crypto payment tool into a major digital payments rail moving value across the global financial system. What started as a way for traders to move between crypto assets now supports cross-border payments, treasury operations, and near-instant digital dollar transfers. The reported $32 trillion in stablecoin transaction volume signals a larger shift: businesses are beginning to treat blockchain-based payments as infrastructure, not experimentation. For companies dealing with slow bank transfers, high fees, or limited access to dollar liquidity, stablecoins offer a faster and more flexible alternative. This momentum is forcing banks, fintechs, and regulators to rethink how money should move in a digital economy.

Institutions are adopting stablecoins because they solve one of finance’s oldest problems: settlement delays. Instead of waiting two or three business days for funds to clear through correspondent banks, companies can move stablecoin payments in minutes, often around the clock. This matters for global suppliers, marketplaces, fintech platforms, and treasury teams that need predictable liquidity without being constrained by banking hours. A business paying contractors across multiple countries, for example, can reduce cash-flow friction by settling in digital dollars instead of relying on slow wire transfers. As a result, stablecoin settlement is becoming a practical tool for improving speed, transparency, and working capital efficiency.

Stablecoins are also gaining traction because they can significantly reduce the cost of moving money. Traditional payment systems often include multiple intermediaries, foreign exchange markups, wire fees, and reconciliation costs, especially in cross-border transactions. By using stablecoin payment rails, companies can streamline transfers and avoid some of the hidden costs built into legacy banking infrastructure. For a business sending frequent international payments, even a small percentage reduction in fees can translate into meaningful savings over time. This cost compression creates competitive pressure on banks, processors, and remittance providers that still rely on slower and more expensive models.

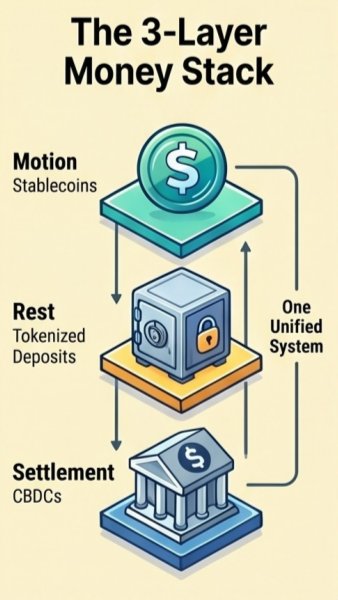

The future of digital money is likely to be built on several connected layers rather than a single payment technology. Stablecoins can move value quickly, tokenized deposits can represent bank-held money on programmable ledgers, and central bank digital currencies could provide final settlement between regulated institutions. Together, these tools create a new money stack that supports faster payments, automated compliance, and programmable financial services. For example, a trade finance transaction could use stablecoins for payment, tokenized deposits for cash management, and a CBDC for wholesale settlement. The key opportunity is interoperability, where different forms of digital money work together instead of competing in isolated systems.

Stablecoins are moving from speculative use into regulated financial infrastructure as policymakers introduce clearer rules around reserves, issuance, and oversight. Regulation such as the GENIUS Act aims to require one-to-one reserves, giving institutions more confidence that stablecoins are backed by high-quality assets. This clarity supports real-world use cases like payroll, trade finance, merchant settlement, treasury management, and cross-border business payments. A multinational company, for instance, could use regulated stablecoins to pay overseas teams faster while maintaining stronger auditability and reserve transparency. As compliance standards mature, stablecoins are likely to become a trusted bridge between traditional finance and blockchain-based payment systems.

Follow the hub for MiCA, stablecoins, RWA regulation, CASP controls and related training resources.

Related Service RWA & Crypto Compliance StrategyPlan regulated token, stablecoin and RWA programs with governance, risk controls and security reviews.

Implementation Use Case Web3 RWA Compliance OperationsSee how teams can coordinate token workflows, compliance evidence and exceptions across regulated asset operations.

Recommended Course Real-World Assets & TokenizationBuild practical fluency in tokenized assets, settlement models, custody, risk and regulatory operating models.

YouTube Playlist Stablecoin & RWA Regulation BriefingWatch the playlist on CLARITY, GENIUS, STABLE Acts, MiCA comparisons and RWA strategy.

Book a Discovery Call Map This to Your RoadmapDiscuss how this topic applies to your product, compliance posture, architecture or delivery plan.

Editorial trust

Each KryptoMindz article is reviewed against current enterprise AI, blockchain, digital identity and compliance practices before publication or major updates.

Founder-led perspective from KryptoMindz Technologies, focused on secure AI adoption, Web3 risk, digital identity and enterprise trust architecture.

LinkedIn profileResearch, engineering and advisory work across secure AI agents, blockchain security, tokenization, compliance operations and digital trust systems.

YouTube channelDiscover more insights and resources on our platform.

Visit Kryptomindz