Is Your UPI Transaction Truly Safe from AI Fraud?

Discover how AI-powered fraud, deepfakes and real-time analytics are reshaping UPI security, and learn what banks, fintechs and users must do to stay protected.

Discover how AI-powered fraud, deepfakes and real-time analytics are reshaping UPI security, and learn what banks, fintechs and users must do to stay protected.

UPI payments are fast, convenient, and deeply embedded in everyday life, but that speed also gives AI-powered fraudsters more room to strike before anyone notices. Rule-based UPI security depends on fixed triggers, such as blocking a transaction above a certain amount or from an unusual location, but modern fraud no longer follows predictable patterns. Attackers can test tiny transactions, rotate devices, mimic user behavior, and automate scams at scale to slip past static checks. For banks, fintechs, and payment service providers, the challenge is no longer just detecting fraud after it happens; it is identifying suspicious intent in real time. This is why AI fraud detection for UPI needs adaptive models that learn from behavior, context, and emerging threat signals.

India’s UPI ecosystem processes massive transaction volumes, creating enormous opportunities for digital financial inclusion, merchant growth, and instant payments. The same scale, however, gives fraudsters a larger attack surface to exploit through phishing links, fake payment requests, mule accounts, and social engineering scams. Traditional banking security still relies heavily on rigid “if-then” rules, but fraud networks now use automation, adaptive AI, and even deepfake-led impersonation to move faster than manual review teams can respond. A scam that begins with one compromised account can quickly spread across multiple banks, apps, and accounts if suspicious patterns are not connected in time. To protect high-volume UPI transactions, financial institutions need intelligent fraud monitoring that can detect both individual anomalies and coordinated attack behavior.

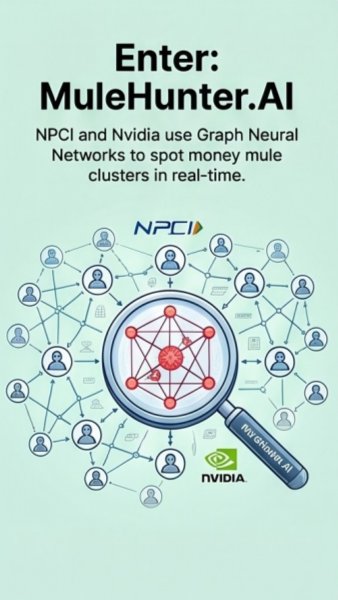

AI-powered UPI fraud detection works by analyzing transaction behavior in milliseconds, long before a suspicious transfer becomes an irreversible loss. Instead of looking only at amount or location, machine learning models evaluate device fingerprints, transaction velocity, payee relationships, login behavior, and historical risk signals. Graph neural networks can map how accounts are connected, helping identify mule clusters, synthetic identities, and unusual fund-routing patterns that basic filters may miss. For example, if several new accounts start receiving small payments from unrelated users and forwarding funds to the same endpoint, AI can flag the network as suspicious before the pattern scales. This millisecond-level intelligence helps banks and payment providers reduce false positives while stopping sophisticated UPI fraud more effectively.

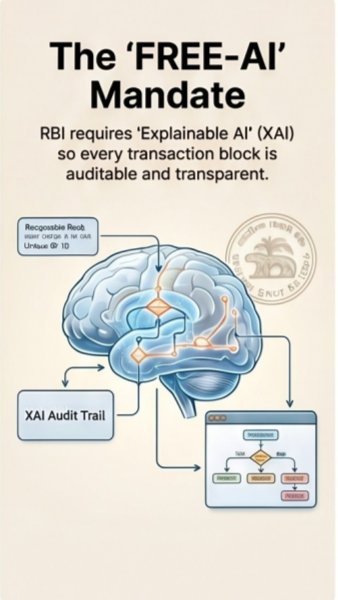

Explainable AI is critical in UPI security because fraud decisions affect real customers, merchants, banks, and regulators. When an AI model blocks or flags a payment, teams need to understand whether the decision was based on device mismatch, abnormal transaction velocity, risky account links, or other measurable signals. Transparent audit trails help compliance teams justify actions, investigate disputes, and meet regulatory expectations without relying on a black-box system. For customer support teams, explainability also makes it easier to resolve false positives quickly and maintain trust in digital payments. In a high-speed UPI environment, explainable AI balances strong fraud defense with accountability, fairness, and operational clarity.

If a UPI transaction feels routine, fraudsters may be counting on exactly that sense of comfort. Smarter fraud campaigns now combine fake customer care calls, malicious links, remote access apps, deepfake audio, and urgency-based messaging to trick users into approving payments themselves. For financial institutions, the warning signs may appear as unusual login behavior, sudden beneficiary additions, repeated small transfers, or activity from a new device. For users, practical safeguards include verifying payment requests, avoiding screen-sharing during banking activity, and treating urgent refund or KYC messages with caution. The future of UPI fraud prevention depends on combining user awareness with AI-driven risk scoring, real-time monitoring, and explainable intervention.

Follow the hub for governed agents, secure tool use, oversight models and AI security resources.

Related Service Secure AI GovernanceDesign AI systems with controls for access, tool use, auditability, escalation and human oversight.

Implementation Use Case Secure AI Compliance Monitoring AgentSee how governed agents can monitor policies, evidence and exceptions without losing accountability.

Recommended Course Secure by Design MandatesTurn secure-by-design principles into practical product, software and operational security controls.

YouTube Playlist Enterprise AI Security ArchitectureWatch the course on secure LLMs, RAG, agents, access controls and AI governance architecture.

Book a Discovery Call Map This to Your RoadmapDiscuss how this topic applies to your product, compliance posture, architecture or delivery plan.

Editorial trust

Each KryptoMindz article is reviewed against current enterprise AI, blockchain, digital identity and compliance practices before publication or major updates.

Founder-led perspective from KryptoMindz Technologies, focused on secure AI adoption, Web3 risk, digital identity and enterprise trust architecture.

LinkedIn profileResearch, engineering and advisory work across secure AI agents, blockchain security, tokenization, compliance operations and digital trust systems.

YouTube channelDiscover more insights and resources on our platform.

Visit Kryptomindz